.webp)

If you have started a new company, you may be entitled to Start-up Company Relief for the first five years of trading.

This relief can be used to reduce Corporation Tax arising on profits from a new trade and on chargeable gains arising on the disposal of assets used in that trade. A company cannot use this relief to reduce Corporation Tax on income and gains which are not related to the trade.

If a company’s Corporation Tax liability is equal to or less than €40,000 in the tax year, the company could possibly be exempt from Corporation Tax in that tax year. If the Corporation Tax liability is between €40,000 and €60,000, the company could possibly be entitled to partial relief.

Any relief available will apply for the five years from the date of commencement. For trades which commenced prior to 2018, this relief applied for three years.

The amount of relief available to a company depends on the employer and director’s class S PRSI paid in the period. The total amount of tax relief available to the company will be the lower of €40,000 and the employer/director’s class S PRSI paid by the company. This will be subject to a maximum employer PRSI payment of €5,000 per employee and class S PRSI payment of €1,000 per director. There is a limit of €40,000 qualifying PRSI in an accounting period.

If a company takes on the activities of another trade while they are claiming this relief, the new trade won’t be considered a qualifying trade. Furthermore, if a company transfers part of a qualifying trade to a connected person, the company will no longer qualify.

XYZ Limited started to trade on 1 January 2024. The company had a 12-month accounting period ended 31 December 2024. The Corporation Tax liability for the tax year 2024 was €30,000. XYZ Limited satisfies all other conditions necessary to avail of Start-up Company Relief.

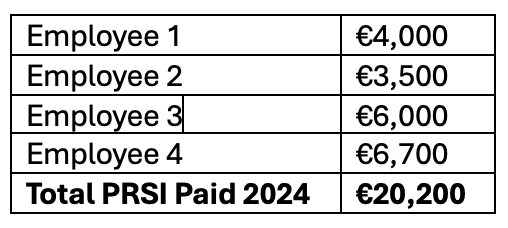

XYZ Limited Employer PRSI contributions paid for the same period were as follows:

XYZ Limited had qualifying PRSI payments in the amount of €17,500 (max €5,000 per employee so only €5,000 would qualify for employee 3 and employee 4). The amount of Start-up Company Relief available to XYZ Limited for the tax year 2024 would be €17,500.

XYZ Limited’s Corporation Tax liability for the tax year 2024 could therefore be reduced from €30,000 to €12,500 (€30,000-€17,500).

It may be possible for a company to carry forward any unutilised relief from:

or

Any unutilised relief available for use in later years must not exceed the total PRSI payments in that year.

A company can apply for this relief through the Revenue Online Services (ROS) by submitting a Form CT1 tax return.

Xero-Awards-IRE-FY25_Email-Signature_Finalist_473x98.png)