Start-Up Relief For Entrepreneurs (SURE) Explained: What Is This Relief And Who Qualifies For It

Elizabeth Kelly FCA CTA

Tax Consultant

About SURE

Start-Up Relief for Entrepreneurs (SURE) is a relief aimed at employees who leave an employment to set up their own company. Where the conditions for the relief are satisfied, the investor can:

claim relief for up to €140,000 as a deduction from their total income in the year of investment

and/or

claim relief against total income in any one or more of the previous 6 years (up to a maximum of €140,000 per year).

This means that it is possible to claim relief for a SURE investment over a seven-year period. The maximum investment for which SURE is available is €980,000 and any unused relief may be carried forward.

In order to qualify for SURE:

The investment must be in a micro/small or medium sized newly incorporated company which carries on qualifying trading activities. It cannot have taken over an existing trade.

The investor must have a minimum share holding of 15% in the company.

The investor must have earned mainly PAYE income in the 3 years prior to the year before the year of investment.

The investor must take up full-time employment in the new company either as a director or an employee.

The investor must invest cash into the new company by means of a purchase of new shares.

The company must use the invested funds within 4 years for the purposes of the trade or research, development and innovation and the funds must also be used towards the creation/maintenance of employment in the company.

The investment must be based on a business plan, which has been prepared in advance of the investment.

The maximum claim for relief which can be given in any one year is restricted to €140,000.

The company must file a ‘Return of Qualifying Investments in a Qualifying Company’ through ROS and issue a “Statement of Qualification (SURE)” to the investor within 4 months of the end of year of assessment in which the shares were issued.

The investor can make a second qualifying SURE investment in the same company within 2 years of making the first SURE investment, if certain criteria are met.

How Does It Work?

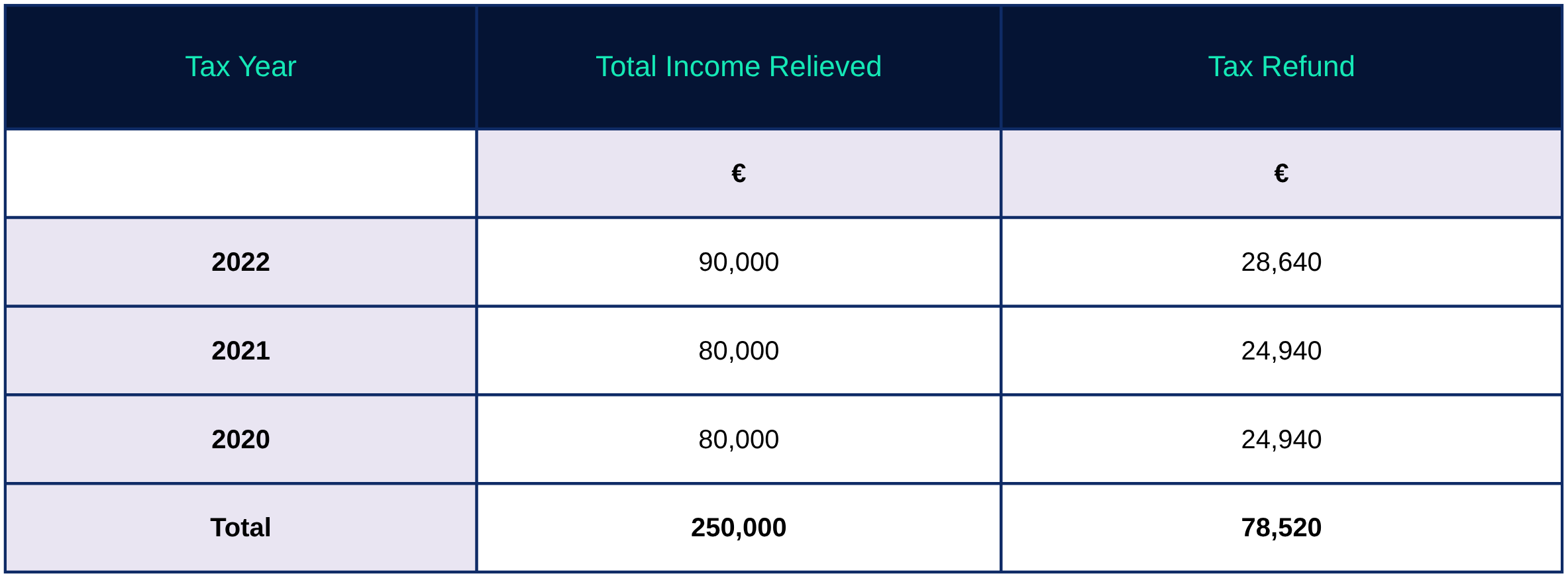

Let’s say Joe incorporated a new company in 2025 and invested €250,000 in the business. His income and Income Tax liabilities for the previous 6 years were as follows:

Joe should elect to claim relief for his SURE investment in the tax years 2022, 2021 and 2020 in order to maximise his tax refund. These are the years in which he had the most income subject to Income Tax at 40%. The potential tax refund due to Joe would be €78,520.

.png)

Xero-Awards-IRE-FY25_Email-Signature_Finalist_473x98.png)